Electrical Appliances

Electrical Appliances Sector

A highly competitive location for outsourcing the assembly of electrical appliances for export to global markets including the USA and EU.

Introduction

Lesotho has an existing electrical appliances

sector based on the assembly of TV sets and

sound recorders.

This project would build on that, taking

advantage of Lesotho’s competitive labour

costs, English-speaking, trainable workforce,

proximity to South Africa and the preferential

access it enjoys to major global markets including the USA and EU, as well as the

Southern Africa region as a member of the

SACU and SADC.

- Electrical Appliances

- Television Sets

- Sound Recording

- Sound Reproducers

Strengths &

Opportunities

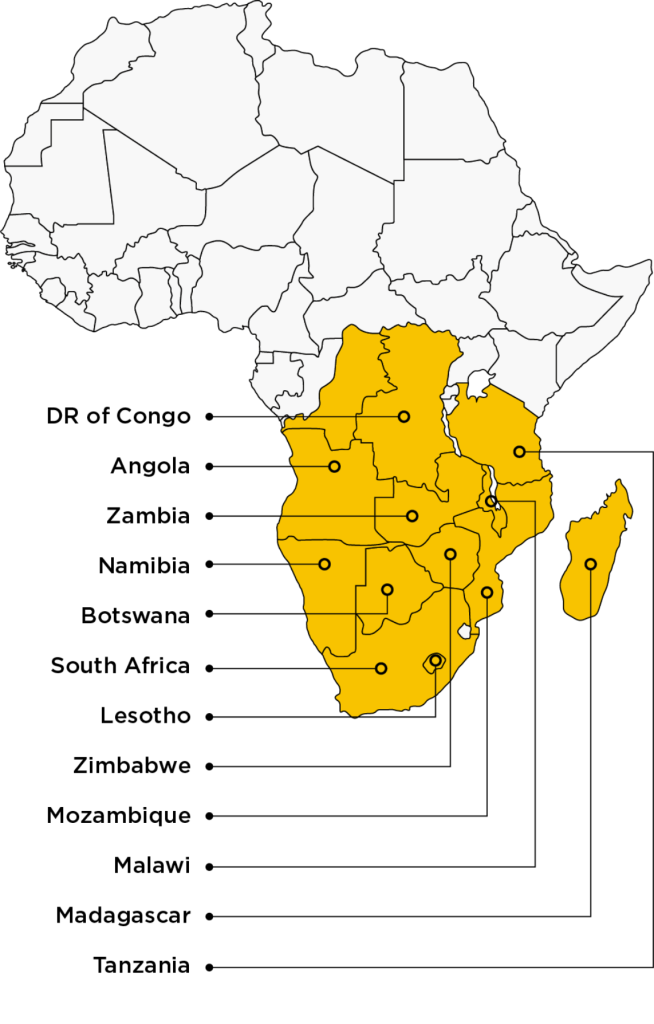

This is an opportunity to diversify the product base and ramp up production levels to serve markets beyond the Southern Africa region.

Lesotho has an abundant and stable labour force with a deserved reputation for manual dexterity. The Lesotho labour force is predominantly young. The literacy rate is 76% and 90% of the population speak English. The majority of the population resides in the lowlands with direct access to the South African road network. Lesotho has relatively harmonious labour relations. In the Lesotho manufacturing sector, wage rates are 20% of the those in the South African sector, making this a highly competitive location for South African OEMs looking to drive down production costs. LNDC rents fully serviced factory shells in industrial estates located near population centres. This helps reduce set-up costs. The industrial estates at Belo near Butha-Buthe and Tikoe near Maseru are potential project locations. Lesotho offers a wide range of attractive incentives to companies setting up manufacturing operations.

These Include:

- A manufacturing corporate tax rate of 10% on profits for intra-SACU trade.

- No withholding tax on dividends distributed by manufacturing firms to local or foreign shareholders.

- No advanced corporation taxes are paid by companies on the distribution of

manufacturing profits. - Training costs are allowable at 125% for tax purposes.

- Payments made in respect of external

management skills and royalties related to manufacturing operations are subject to withholding tax of 10%. - Easy repatriation of manufacturing profits.

- A VAT rate of 15% (ensuring harmonisation with the RSA). Furthermore, the Lesotho Revenue Authority has introduced flexible

VAT payment systems, for tax compliant firms, to ease cash flows.

The project aligns with SDGs 1, 8, 9 and 10.

to the US market under the African Growth and Opportunity Act (AGOA). In practice it only exports a small fraction of these product lines. AGOA-eligible products include electrical machinery.

As a Less Developed Country, Lesotho benefits from preferential market access to the EU under the EU/SACU EPA; EFTA; MERCOSUR; and with a wide range of countries under the Generalised System of Preferences (GSP), including China.

Lesotho also can utilise inputs from other countries benefiting from China’s LDC preferential scheme.

These agreements give Lesotho an important comparative advantage in relation to more developed exporters.

Lesotho’s access to both regional and North American markets is well established in terms of logistics. The external road connections via South Africa are excellent. Access to the port of Durban for Lesotho made products is straightforward. Shipments from Lesotho take from 18 to 23 days to reach a US port.

Project Assumptions

The immediate opportunity is for companies based in South Africa to outsource parts of their value chain to nearby Lesotho. But there are also openings for companies from outside the region to invest in manufacturing in Lesotho.

Training the workforce is an important consideration. South Africa offers a wider range of facilities for education and training than Lesotho. But the workforce is trainable and training costs can be offset against tax.

Belo Industrial Park, Butha-Buthe.

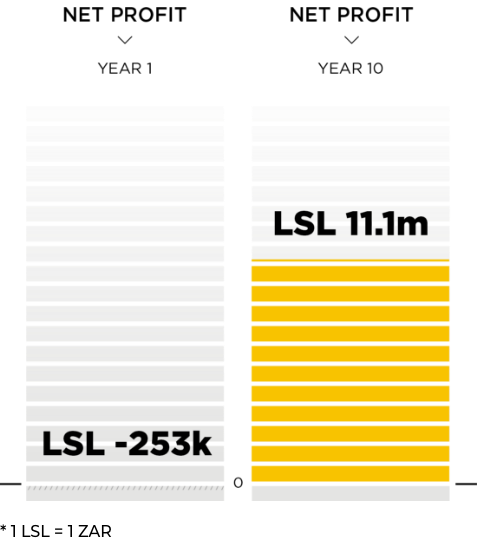

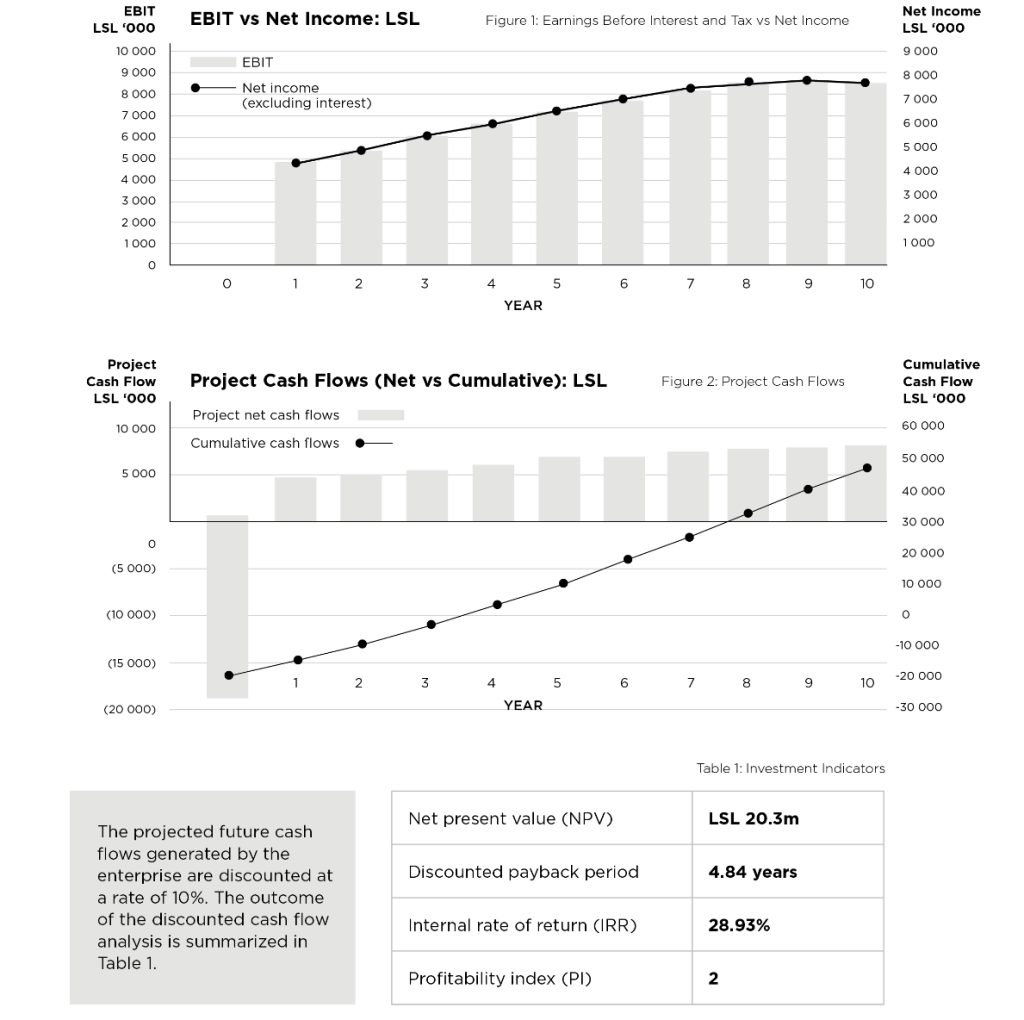

Financial Analysis

A total investment of approximately:

Financial Analysis

Mabataung Tsinyane

Manager: Investment Promotion, Manufacturing

Lesotho National Development Corporation

Email: [email protected]

Makopano Mosakeng

Officer: Investment Promotion, Manufacturing

Lesotho National Development Corporation

Email: [email protected]

Tsepiso Mofolo

Officer: Investment Promotion, Manufacturing

Lesotho National Development Corporation

Email: [email protected]